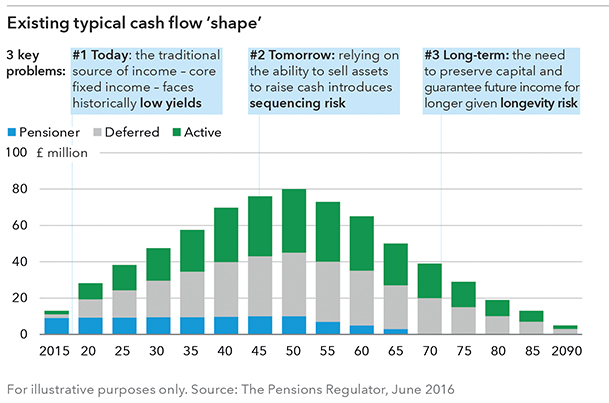

Defined benefit (DB) pension schemes are rapidly moving into cash flow negative territory. As their members grow older, it's time to make good on those pension promises.

Unfortunately, we find ourselves in an ultra-low yield environment – the flow of income that gilts and corporate bonds traditionally provided has slowed to a trickle. A gap has emerged between the cash flow required and that being generated. The new challenge for DB pension investment is thus not: what are the liabilities of the scheme; but how will those liabilities be paid, now and in the future?

Moving from a balance sheet to a cash flow approach

When considering the income that assets need to generate, there are broadly three main issues to address:

1. Cash flow today – Today's ultra-low yields, compressed by central bank intervention in markets and increased demand from pension funds, are forcing investors to look further afield. This is especially the case once schemes turn cash flow negative and need to start selling assets. Some investors have focused their attention on alternative fixed-income assets such as infrastructure debt. However these are often illiquid, capacity - constrained and expensive to access.

2. Cash flow tomorrow – So why not simply begin selling assets? Unfortunately this leaves you at the mercy of markets; if you need to raise cash to pay an income, you risk becoming a 'forced seller' – having to accept whatever the market price is for your assets on that day. This is known as 'sequencing risk' – if you have to sell assets the day after the market has taken a downturn, you risk permanently impairing your capital pot, giving you fewer assets to generate an income from in the future.

3. Cash flow for the long term – Improving longevity poses an ever greater risk to pension funds – can the assets last long enough to provide an income to your healthiest pensioners? If you have had to sell assets rather than just taking an income from them, there is a stark danger that the pension pot may simply run dry.

Look at your assets in a new light – do they generate income?

It's clear that we need a new framework for thinking about the purpose assets serve within a portfolio. In a 'lower-for-longer' interest rate environment, these risks are persistent, and capacity - constrained alternative assets such as infrastructure or private debt can only partially close 'the income gap'.

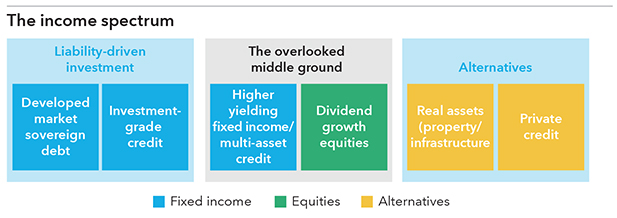

In our view, the answer is to reconsider the role that all of your assets play in income generation – and particularly 'the overlooked middle ground'. These are the higher-yielding areas of fixed income as well as equities – a 'risky' asset class that has been out of favour with pension schemes for a considerable period. In an environment where certain good-quality equities offer greater yield than investment-grade bonds, as well as future growth potential to counter mortality risk, it may be time to reconsider what is a 'risky asset' based on what it can do to counter the cash flow challenge. By diversifying your sources of income in the same way you diversified your liability matching and growth assets, you could find a sensible solution to closing the income gap.

Equities – really? But what about the volatility?

'De-risking' has been the fashionable goal in pensions for a long time, so to consider equities as part of the solution may feel like an uneasy answer. But let's consider the question of volatility – in equities the movement tends to come from the capital return rather than income return; the income stream can be robust and consistent as long as short-term capital movements can be tolerated. It also depends on the type of equity – dividend-paying equities tend to be less volatile overall. By repurposing growth assets to dividend-paying equities, the overall volatility of the funding ratio could potentially be reduced.

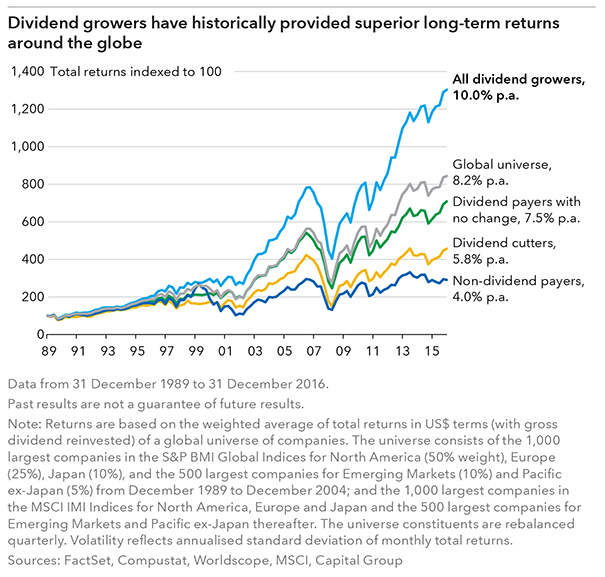

Furthermore, dividend-paying stocks have demonstrated greater resilience than their non-dividend- paying counterparts in bear markets and lower volatility overall, making a significant positive impact on cumulative investment returns over the long run (see chart below). Evidence also shows that companies that have been able to grow their dividends over a number of years have generated superior total returns compared with those that pay flat dividends, declining dividends or no dividends at all. Growing dividends over time tends to be a sign of good allocation of capital; the need to pay dividends may mean that company managers select only the highest returning projects.

The role for equities in tackling longevity and inflation risk

As lifespans expand, asset classes like equities that can be owned over the long term and do not carry reinvestment risk have clear advantages. In addition to current dividends, equities offer the potential for dividend distributions to grow in the future and for capital values to increase. Although inflation may currently seem a distant prospect, the potential for a degree of inflation protection through owning the rights to earnings from productive assets has a long-term attraction.

In summary, with many UK DB pension schemes becoming increasingly mature and moving to cash flow negative territory, there is a need to reconsider investment strategy and to prioritise income and cash generation rather than simple capital appreciation, or return over a benchmark. We would suggest that the 'overlooked middle ground' could offer income – indeed, in many cases yields that are higher than bonds– without compromising on liquidity, transparency and capacity.

Although equities are generally more risky than bonds, this could be mitigated to some extent by adopting a strategy that invests in dividend-growing equities rather than simple 'high yielders'. This approach has historically exhibited less volatility than equity markets in general and has held up well in down markets, making it particularly attractive for pension schemes that need to liquidate assets on a regular basis.

Company profile

Founded in the US in 1931, Capital Group is one of the world's largest independent investment managers. Throughout our history of more than 80 years, our aim has always been to deliver superior, consistent results for long-term investors.

Investment management is our only business, and the stability of our privately owned organisation has enabled us to maintain a long-term perspective throughout the decades; we believe this perspective helps to align our goals with the interests of our clients. The majority of our portfolio managers and analysts have witnessed several market cycles and have been with Capital Group for many years.

We build our investment strategies with durability in mind, backed by our experience in varying market conditions. Our active investment process is designed to enable individual investment professionals to act on their highest convictions, while limiting the risk associated with isolated decision-making. Fundamental proprietary research provided by our global network of experienced investment analysts forms the backbone of our approach.