Pensions Freedoms – have you implemented your 7 Point Plan?

Friday, November 20, 2015

DB savers want the same freedoms as DC savers; Richard Smith explains how to prepare for this.

It's been seven months since the new pensions freedom flexibilities came into effect, which completely re-drew the landscape of retirement savings.

During that period, around GBP 5 billion of cash has been withdrawn from the pensions system, both from cashing in small pots and drawing income out of larger ones.

However, with an average "cash-in" value of around GBP 15,000, Lamborghini dealers are still waiting to join the party.

Concerns about profligate retirees blowing their retirement savings have so far not come to pass.

General feedback from the industry is that people tend to be quite sensible in the decisions they are taking over their retirement income.

This is not particularly surprising – it seems a little unlikely that someone who has saved all their working life would suddenly spend the lot as soon as it become accessible; hard-working savers deserve more credit than that.

There has been so much media coverage of the new freedoms over the last year or so, not to mention auto-enrolment and the ubiquitous "Workie", that the level of public awareness of pensions has probably never been higher.

However, one theme that I hear over and over again from my clients is that their defined benefit (DB) membership doesn't always appreciate that these freedoms don't apply to them.

Having been told by the media that they can take their pension as flexibly as they would like, it is an unpleasant surprise to then be told no – those new rules don't apply to you.

Defined contribution (DC) members are considered to be sensible enough to be trusted with their retirement monies, but DB members are stuck with an inflexible annuity paid from their scheme.

In recognition of this unfairness, and in light of unprecedented demand from DB members, more and more trustees are enabling their members to transfer their benefits out of the scheme in order to access the pension flexibilities.

Administrators across the country are reporting significant increases in transfer value quotations.

Unsurprisingly, there is a surge of interest in transfer exercises from employers spotting the opportunity of a win-win-win for members, trustees and the corporate finances.

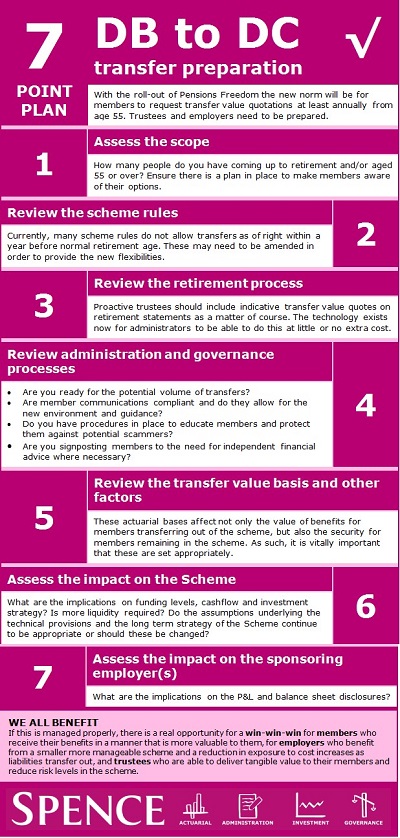

Back in March, Spence developed a 7 Point Plan to ensure trustees and sponsors were prepared for the anticipated surge in demand which has now materialised.

Now we are a few months into the new regime and things are settling down to a new normal, it seems a good time to take stock and check your processes are aligned with the trustees' and corporate objectives.

Here is the 7 point plan – how do you measure up?

Richard Smith, Head of Corporate Advisory Services, Spence & Partners